Are you struggling to keep your company afloat? If you said yes, you’re not the only one who feels this way. Many businesses were on the verge of bankruptcy as a result of the pandemic. Companies are shutting down at alarmingly high rates. Small businesses were failing due to a lack of consumer foot traffic.

And while these may seem discouraging, some businesses faced financial challenges but were still able to overcome them. If your company is struggling financially and you want to keep it open, here are some tips you can consider to avoid bankruptcy.

Tips to avoid bankruptcy and save your business

1. Analyze your financial Situation

One major reason for business failure is insufficient cash flow. To tackle this problem and avoid bankruptcy, you must first figure out how much cash flow your company actually needs. There are various tactics you may employ to enhance your cash flow, including paying invoices on time, borrowing money before cash flow becomes an issue, and rescheduling your payments.

2. Try to ask for flexibility or new terms with your suppliers

Vendors, like you, want to continue in business. Many businesses are eager to bargain for cheaper costs rather than lose a loyal customer. If you acquire supplies on credit and fall behind on payments, explain your situation to your suppliers or merchants. They may be prepared to work out a payment plan or reduce your costs. If you have a solid relationship with your vendors and suppliers, they will have an incentive to keep your business as a client.

3. Communicate with lenders promptly

If you can’t make business loan payments on time, contact your lenders immediately. Falling back on a loan can result in a reduced credit score, late penalties, and a lawsuit filed by the lender for the amount outstanding. By promptly contacting your lenders and explaining your position, you may be able to prevent default. Your lenders could be ready to put the loan on hold, extend the term, or work out a payment plan with you.

4. Learn to prioritize your debts and payables

While all obligations must be paid, there are some that are more crucial than others. Make a list of your bills and prioritize them so you know which ones to pay first. Taxes, which include income, payroll, and property taxes, are some of the most important debts for small businesses. Because tax money belongs to the government and not to your company, it should be your first focus. Payroll is your second priority, and any bill that is 60 days or more past due is your third.

5. Cut costs

To stay in business, you will likely have to reduce your costs. There are many ways to cut business costs. First, reduce your supply expenses. Look outside your pool of traditional vendors and try to price shop. Always search for ways to reduce material expenses and maximize your resources. You can search for savings opportunities in your insurance coverage and financial accounts. Don’t take on debt that you don’t need. When planning a business expansion, conduct a detailed cost-benefit analysis and forecasts. Reduce utility costs and review your equipment leases. Make use of technology to reduce expenses.

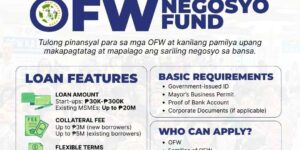

6. Take Advantage of Government Programs

Several government programs are offering loans, training, and financial assistance to help businesses affected by the pandemic. You can look into:

- Bayanihan Cares‘ Pondo sa pagbabago at pag-asenso (P3)

- COVID-19 pondo para sa pagbabago at pag-asenso enterprise rehabilitation fund (P3 ERF)

- LandBank’s Rehabilitation support to cushion unfavorably affected enterprises by COVID19 (I-RESCUE).

- IT Engineer Quits Job To Sell Siomai, Now Earns P5,000 A Day - June 30, 2023

- From Chocolate Cakes To Noodles: Maricar Reyes’ Food Businesses - June 25, 2023

- How To Be A Cebuana Lhuillier Authorized Agent - June 17, 2023